'%3e%3cpath%20d='M29.3373%2096.1258C16.4488%2096.1258%206.86376%2083.4535%206.86376%2067.6711V67.0051H47.5157V65.3385C47.5157%2050.7767%2039.2539%2041.1089%2027.5751%2041.1089C13.8054%2041.1089%203.11816%2054.7818%203.11816%2070.6757C3.11816%2084.457%2011.1589%2099.5734%2027.4645%2099.5734C40.1321%2099.5734%2047.7338%2090.3487%2051.2583%2078.7884H49.6066C44.8693%2090.3487%2038.0382%2096.1288%2029.3373%2096.1288V96.1258ZM27.133%2044.5535C37.0466%2044.5535%2042.7755%2052.2232%2042.7755%2063.672H7.41335C8.9546%2053.0007%2016.6668%2044.5535%2027.133%2044.5535Z'%20fill='black'/%3e%3cpath%20d='M60.0131%209.42966H55.6074V98.3498H60.0131V9.42966Z'%20fill='black'/%3e%3cpath%20d='M77.7944%209.42966H73.3887V98.3498H77.7944V9.42966Z'%20fill='black'/%3e%3cpath%20d='M111.394%2096.1258C98.5054%2096.1258%2088.9204%2083.4535%2088.9204%2067.6711V67.0051H129.572V65.3385C129.572%2050.7767%20121.311%2041.1089%20109.632%2041.1089C95.862%2041.1089%2085.1748%2054.7818%2085.1748%2070.6757C85.1748%2084.457%2093.2156%2099.5734%20109.521%2099.5734C122.189%2099.5734%20129.79%2090.3487%20133.315%2078.7884H131.663C126.926%2090.3487%20120.095%2096.1288%20111.394%2096.1288V96.1258ZM109.19%2044.5535C119.103%2044.5535%20124.832%2052.2232%20124.832%2063.672H89.47C91.0112%2053.0007%2098.7235%2044.5535%20109.19%2044.5535Z'%20fill='black'/%3e%3cpath%20d='M176.004%2042.7725H172.811L157.939%2066.4475L142.076%2042.7725H136.126L154.522%2070.3381L135.684%2098.3468H138.769L156.284%2072.8937L173.692%2098.3468H179.639L159.591%2069.0061L176.004%2042.7725Z'%20fill='black'/%3e%3cpath%20d='M208.831%2069.0061L225.247%2042.7725H222.051L207.179%2066.4475L191.315%2042.7725H185.368L203.765%2070.3381L184.926%2098.3468H188.012L205.527%2072.8937L222.932%2098.3468H228.882L208.831%2069.0061Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_35_103'%3e%3crect%20width='232'%20height='109'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

«Most money mistakes aren't mathematical. They're emotional»

Money seems to be the very epitome of rationality. Yet you write that most of our financial decisions are driven by emotion. So which is it?

We just haven't been taught to look at money through an emotional lens. There's also this cultural idea, in economics, in politics, that incentives drive behaviour and everyone responds rationally. But most money mistakes aren't mathematical. They're emotional ones. I sometimes hear young people say, «I'm bad with money because I'm bad with maths.» But how are those related? A spreadsheet or an app does the calculations. The mistakes happen elsewhere.

Where do people notice that their money choices aren't always driven by ratio?

We might spend too much on a gift and not quite know why. We might spend compulsively on ourselves without understanding what's driving it. We might feel guilty giving ourselves good things – and we can't figure out why.

Why do we keep treating money as a «rational» topic?

we still assume people will be rational about money. As if, with the right information, they'll automatically act in the «right» ways. That's a myth that's been around for a long time. In investing, there's been more attention on why people don't act rationally; behavioural finance exists because there was a lot of money to be made understanding investor behaviour. But in personal finance, the penny hasn't dropped yet.

Emotions are often devalued in our society. What are the consequences of that when it comes to money?

I'd agree. And it doesn't help anyone – not women, and not men either. The men I end up seeing can be full of shame because they've done something «wrong» in their personal finances. Some are CEOs or CFOs in their day job – but privately they've made an absolute mess. And they feel: Aren't I supposed to be good with money? I'm a man, I'm successful – how did I do this? When we normalise that this isn't about being bad at your job or «less of a man», but about being a human being – an emotional human being – it changes things.

One concept that really hits in your book is self-sabotage – the feeling of having to spend until there's nothing left. Can you explain this concept to us?

The key question is: What am I gaining by sabotaging my finances? Often there's a good psychological rationale. Sometimes it's peace: «Now I have nothing, so I don't have to feel guilty about having.» Sometimes it's the pleasure of being rescued – and feeling looked after. A client of mine kept running out of money each month. I assumed overspending – until I asked: What happens when you run out? They said: «I call my dad.» Then: When else do you speak to your dad? «That's the only time we talk.» Suddenly it made sense: sabotaging their finances kept a relationship alive. We're not «mad.» Usually there's an underlying psychological driver.

Vicky Reynal

Is there a «typical» client?

They vary a lot – from ultra high net worth to people I see on a concession fee who pay very little because that’s what they can afford. It varies by gender too. Before I focused on financial psychotherapy, I saw more women. After, more men started coming. For some older men, calling it «financial» psychotherapy reduced the shame of seeing a therapist. And men often carry a culturally imposed burden to provide. When that goes wrong, or they don’t fulfil their expectations of themselves, there’s huge shame and responsibility – so having a place to talk is a relief. Clients are international too – I have people from Singapore to Tennessee, and yes, also a few in Switzerland.

Vicky Reynal

There's a lot of shame involved in bad financial decisions. What does shame do to people in financial hardship?

Shame keeps people stuck. Take debt. A lot of people don't attend to debt – even knowing that the earlier they intervene the better – because facing it might feel like they have to accept they have failed (and are a failure), or that they will lose respect in the eyes of others. So the problem spirals and gets worse. I don't think shaming people is the way out. We all make mistakes and no one has it all figured out when it comes to money. But often not having been taught enough personal finance we are left with no compass to navigate financial choices and crippled by insecuirities.

How can we work our way out of shame?

We can't change what happened – but we can change what we do next. And often, our worst critic is ourselves. People imagine others will judge them – but often that's not the case. I've worked with people who keep money secrets from their partner. The fear is: «She'll leave me. She'll never forgive me.» But eight times out of ten, the other person is much more understanding. They appreciate the honesty – even if it came late. That helps people move out of shame and into action. Trying to turn shame into guilt is key: the debt might have been related to mistakes we made, but that doesn’t make us a failure. Guilt is about what we did, shame is about what that “makes us”… they are different in an important way: we can learn from mistakes and move on, but shame keeps us stuck in a self-depricating place.

Vicky Reynal

Most money stories seem to lead back to childhood. Is that too simplistic?

A lot of it does – but not all of it. People also have major experiences later – bankruptcy in their late twenties, for example – that can dramatically change their relationship with money. What gets shaped in childhood is our personality, our deepest fears and desires: are we generally anxious or impulsive? Do we fear intimacy or rejection? Those patterns come from early relationships with caregivers – and they can shape how we manage money.

Can you give an example of how childhood experiences shape the way we handle money?

Sometimes people orchestrate self-sabotage so they can be rescued, because being rescued makes them feel cared for. Others grow up with scarcity and become workaholics, trying to make sure they never long for anything again. There are deeper forces too: if home was unstable – parents with addiction, abusive parents – that baseline anxiety can show up in finances: always afraid the money won't be there. Or competition between siblings can create a scarcity mindset: not enough love, not enough money – if someone else has, I can't.

Vicky Reynal

You also write about people who feel they don't deserve money. Where does that come from?

Some people can't even pay for a massage without guilt. When you unpick it, there's a part of them that never felt deserving – often tied to early experiences like a depressed or absent parent, where they didn't get that feeling of «your presence delights me», which builds self-esteem. When we don’t have enough experiences, growing up, of the world responding positively to us, as young children we assume that it must be because there is something wrong, or underserving about us. With that internal landscape, it is hard to then, as adults, feel deserving of good things (like money, or the good things money can buy).

Vicky Reynal

Parents want to teach children «financial literacy». But your point is: it's not just rational knowledge. So what can parents do?

The key word isn't only financial literacy – it's financial emotional awareness. Help your child notice what they feel when making money decisions. Start early, when pocket money begins. One child might spend it all immediately on a Lego set. Give them the freedom – and then be curious: How does it feel? «Great, I'm excited.» Let them connect to that. Then they might see a sibling saving and feel envy. Name it gently: Are you envious? That's emotional literacy.

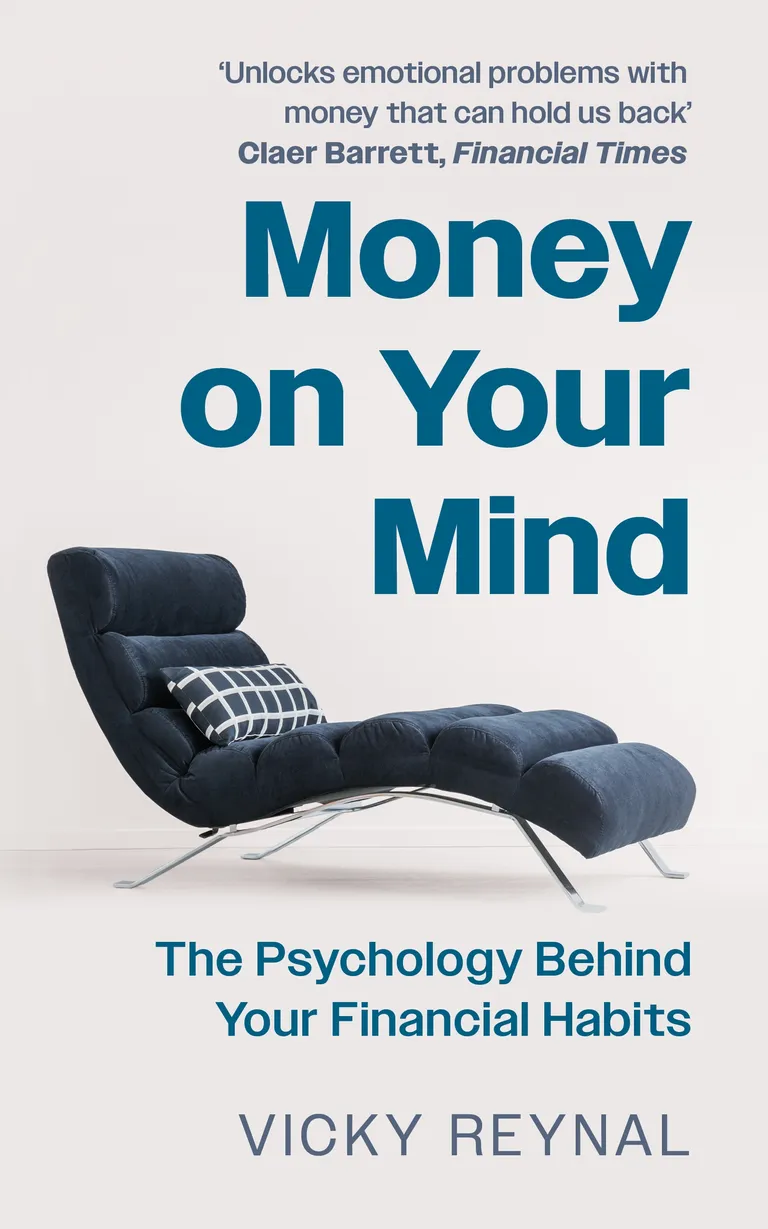

Vicky Reynal is a UK-based psychotherapist who specialises in the emotional side of money. Trained in psychotherapy, she also holds an MBA from London Business School.

Vicky Reynal's book

Money on Your Mind. The Psychology Behind Your Financial Habits, Bonnier Zaffre, 2025

Many money problems aren't just personal – they're structural, shaped by our economic and political systems. There are significant wealth disparities between the genders. How do you hold both realities at once?

There are advisory firms that pay lip service to women – they know the next big wealth transfer is to women, so they want to «welcome» them. But are they truly creating women-friendly practices, or still approaching everything from a male perspective? I read a report recently that said: stop saying the issue is female confidence. Even with confidence, walking into a system designed by men and led by men is hard.

Women had limited financial autonomy historically. Do you see that as a kind of transgenerational «blueprint»?

We need to adapt to new dynamics, especially in relationships. We may feel we deserve equal say in decisions and equal sharing of childcare because we both work – but it doesn't always happen. Do we sometimes become complicit and settle into familiar dynamics? A part of us gravitates to what's familiar – what we saw our mothers do – and another part wants to assert itself and demand a new balance. Those blueprints take generations to change.

Vicky Reynal

I feel like there's new pressure now on women – like they have to earn more, invest more, just to not be a burden. Just learn how to invest already!

Women feel: «I don't invest because I don't know how – but I know I should.» The content is endless. The shame rises. I hate to generalise, but women often tend to be more conservative; men a bit bolder. Does everything have to be equal – or can differences be complementary? Maybe women think longer-term, more about the safety of the family. Can we shape a financially empowered way of being that isn't «doing it the men's way»? It's confidence-building, yes – but also addressing insecurities and biases we're not aware of. Sometimes we're unconsciously biased against ourselves. It's much more than knowledge.

What drew you personally to this topic?

My family had a difficult, complicated, dramatic history with money. I benefited from talking about it in my own therapy. It helped me understand why people made the decisions they made. I saw I was afraid of the same things happening again. And I learned how to be more conscious so I wouldn't repeat mistakes. It helped me massively – and I wanted other people to have that experience too.